What to Do If You’re Hit by an Uninsured or Underinsured Driver

Car accidents can be stressful, dangerous, and incredibly inconvenient. It’s hard enough to deal with the aftermath of a crash, and when the at-fault driver has no insurance or insufficient coverage, the situation becomes even more complicated.

That’s where uninsured or underinsured motorist (UM) coverage comes in. If your policy includes this coverage and your accident qualifies, it can help protect you from financial fallout.

What is an uninsured or underinsured motorist?

An uninsured motorist is a driver who causes an accident but does not have any auto insurance. An underinsured motorist is a driver whose insurance coverage is not enough to pay for all the damages from an accident.

In 2023, 15.4 percent of drivers were uninsured, meaning more than one out of every seven drivers on the road had no coverage at all, according to a 2025 Insurance Research Council study. The study also found that uninsured driving increased in most states between 2017 and 2023, with many states in the Southeast reporting above-average rates.

Being involved in a crash with an uninsured or underinsured driver can leave you responsible for medical bills, lost wages, or car repairs if you don’t have the right coverage. That’s why UM coverage is so important. In the event of an accident, this coverage can step in to help protect you financially when the at-fault driver doesn’t have enough insurance to do so.

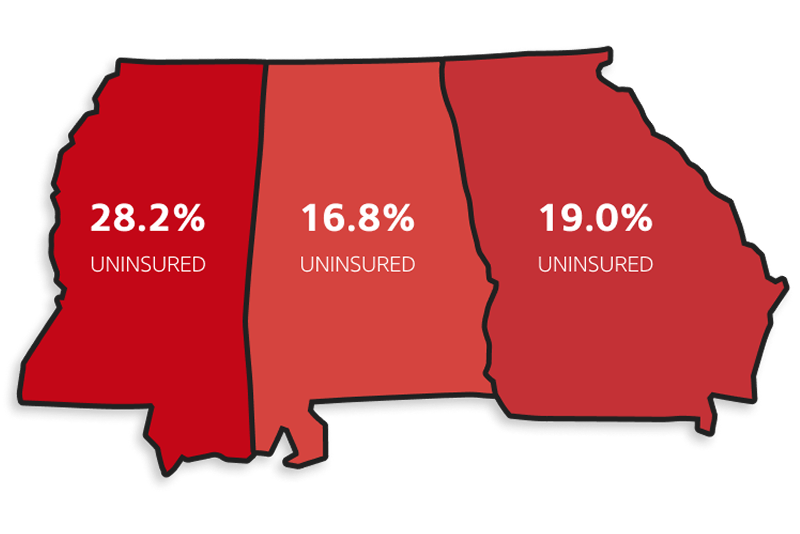

Uninsured motorist rates in Alabama, Georgia, and Mississippi, according to a 2025 study by the Insurance Research Council

Practical steps to take after a car accident

1. Call the police

Filing a police report is essential, even if the accident seems minor. Documentation is crucial to prove who caused the accident. Do not let the other driver convince you otherwise. Stay at the scene, call 911, and wait for help to arrive. Take clear photos of all vehicle damage and the accident scene for your own records.

2. Stick to the facts

It’s natural to want to explain or apologize after a crash, but keep your statements factual and neutral. Avoid emotional phrases such as “I’m so sorry this happened,” because they could be interpreted as an admission of fault. Only share the necessary details about what occurred. You don’t want to accept any liability for the accident if you are not at fault.

3. Contact your insurance company

Let your insurance company know about the accident as soon as possible. Your agent can guide you through the claims process. Early communication ensures your claim is handled smoothly and avoids unnecessary delays.

4. Get a medical exam

When you’re in a car accident, adrenaline can hide pain or injuries, and you might not notice them until hours or even days later. Even if you feel okay, it’s important to get a medical exam. A thorough evaluation not only ensures your health and safety but also provides documentation that can be crucial when filing a claim.

What can uninsured and underinsured motorist coverage cover?

UM coverage is often more affordable than many drivers expect and can provide protection after a covered accident. Coverage options, limits, and eligibility can vary by state, so it’s important to review your policy carefully.

Here’s how this coverage may apply:

Bodily Injuries

If you’re injured in an accident caused by an uninsured or underinsured driver, UM coverage can help pay for medical bills, lost wages, and other related expenses.

Hit-and-Run Accidents

If you’re involved in a hit-and-run and the responsible driver cannot be identified, UM coverage can help cover your losses.

Property Damage

UM coverage can help pay for damages to your vehicle or other property when an accident is caused by an uninsured or underinsured driver. However, property damage coverage is only available in select states, such as Georgia and Mississippi, and is currently not offered in Alabama.

Protect the unexpected.

For peace of mind on the road, it’s a good idea to review your uninsured and underinsured motorist coverage. Doing so can help you identify any gaps in your protection and understand how your policy responds in different accident scenarios. Consider speaking with an Alfa Insurance agent, who can help you explore your options, answer questions, and ensure your policy provides the protection you and your family need.

All coverages are subject to deductibles and policy limits. This is not an insurance policy. It is intended only to provide a general description of Alfa Insurance® and/or its product lines and services. An actual policy contains the specific details of the deductibles, coverages, conditions and exclusions. Your Alfa® agent can explain the policy and benefits and answer any questions you may have before you buy.